CJ ATKINS takes a closer look at Trump’s recent spate of red-baiting speeches and asks why the authoritarian president is running scared

‘Civilising a hugely irrational world’

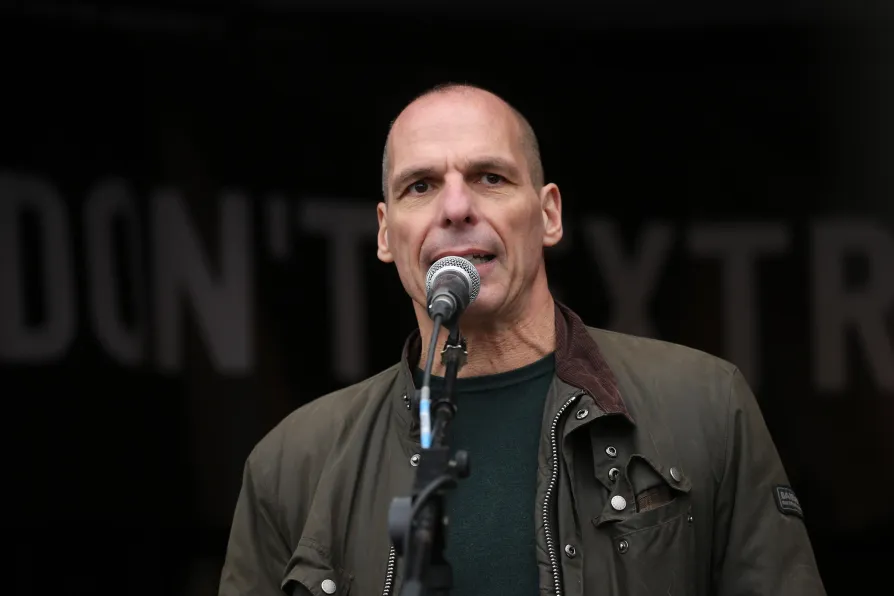

The former Greek finance minister for Syriza YANIS VAROUFAKIS speaks to Daniel Powell about Brexit, ‘techno-feudalism’ and how social media users could generate a universal basic income for all

JOHN McINALLY sees little chance of change at Westminster, and calls on the left to get serious about building a real alternative

With the centenary of the UN Slavery Convention upon us, ROGER McKENZIE argues much needs to be done to rid us of all its contemporary manifestations

SEVIM DAGDELEN says European Nato states are escalating ever closer to direct conflict with a nuclear power, and sacrificing welfare states built up over a century to finance it

CLAUDIA WEBBE says the horrific price British patients will pay for this NHS deal is now clear — and there’s time to get out of it, if MPs will only force the issue

KENNY MacASKILL says the lines between party, government and Civil Service in Scotland have been blurred and we need a thorough investigation into how

ONE YEAR since the final deal for Brexit was announced, it remains one of the most divisive political subjects for a generation. Perhaps unknown to most, the incendiary B-word had its genesis in the term “Grexit” — coined during tumultuous years after the 2008 credit crunch when a Greek exit from the EU was speculated, as the nation’s people suffered punitive austerity measures imposed by the “troika” of EU Commission, central bank and IMF.

After subsequent periods of mass civil unrest, rioting and national catastrophe, the democratic socialist party Syriza was elected in 2015, with Yanis Varoufakis serving as finance minister during crucial crisis talks with the deep establishment of the EU, as dramatised in the 2019 movie Adults in the Room.

Varoufakis became a familiar face in British media during the Brexit period and expresses dismay concerning some of the dogma surrounding the debate.

Similar stories

As the dollar falters and US power turns predatory, Britain and Europe must abandon transatlantic illusions and build a collectivist alternative before the system implodes, writes ALAN SIMPSON

Politicians who continue to welcome contracts with US companies without considering the risks and consequences of total dependency in the years to come are undermining the raison d’etre of the NHS, argues Dr JOHN PUNTIS

Starmer sabotaged Labour with his second referendum campaign, mobilising a liberal backlash that sincerely felt progressive ideals were at stake — but the EU was then and is now an entity Britain should have nothing to do with, explains NICK WRIGHT