Special report by PEOPLE’S WORLD

Ten years after the financial crash: the decade of a rising China

NICK WRIGHT considers how the isolation of Israel and a new film on the controversial Italian communist leader are creating new reference points for Italy’s left

CARLOS MARTINEZ says Cuba’s achievements in the face of a criminal blockade are startling, but the island’s future if the United States succeeds in crushing it looks bleak

AMNON BROWNFIELD STEIN reports that far-right MPs who mobbed the event organised by Hadash may have helped raise awareness of the brutality of the Israeli right

Born on this day in 1931, the heroic revolutionary faces a dangerous new wave of White House aggression. We must treat his birthday as a rallying cry to resist the illegal siege of Cuba, writes ROGER McKENZIE

RAMZY BAROUD decries the rats of Gaza, the rodent and human type. Both abound as profiteering from tragedy reaches obscene levels

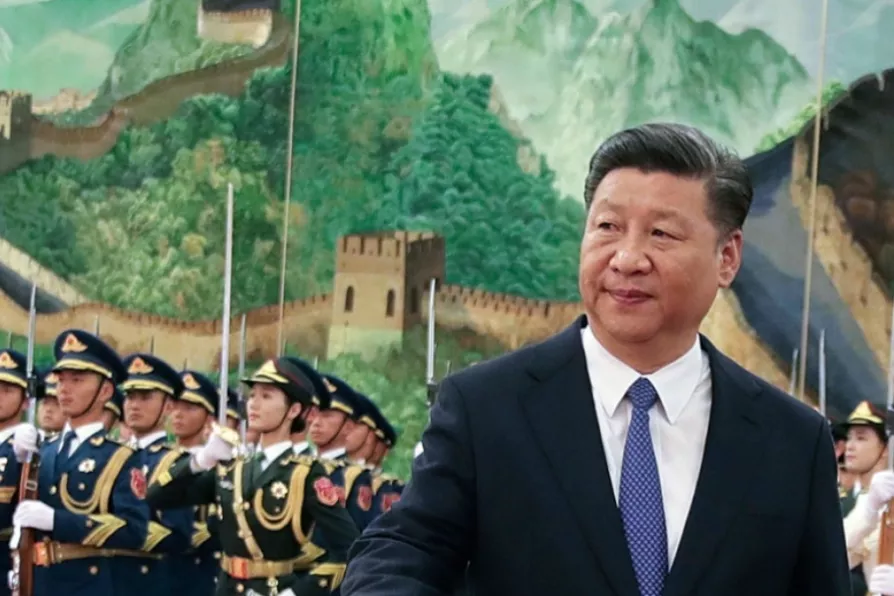

IT IS 10 years this September since Lehman Brothers went bankrupt, bringing global capitalism to the point of collapse.

Although a total meltdown was avoided, the crash triggered a slump of 1930s proportions, and for most economies the last decade has been a lost decade of low growth, low investment, low productivity, debt, deficit, with virtually no improvement in real incomes for the 90 per cent.

The stand-out story of the period has to be the continuing rise of China. Initially also badly hit by the crisis, China recovered rapidly to emerge today as a major economic power, moving steadily closer centre stage in the global order.

Similar stories

Coal-fired stoves in traditional homes are the primary source of extreme levels of air pollution in over-crowded Ulaanbaatar. As more people become climate-displaced, the situation is likely to worsen, write SCIENCE AND SOCIETY

As the Global Leaders’ Meeting on Women begins in Beijing, it’s clear that China has fulfilled its commitments set 30 years ago and delivered amazing progress in women's education and equality, writes YU BOKUN

It’s the dramatic rise of China with its burgeoning economy that has put the Trump administration into a frenzy – with major implications both at home and abroad, argues MICHAEL BURKE

Under current policy, welfare cuts are just a small downpayment on future austerity, argues MICHAEL BURKE